WHY THIS CHANGED: SUPREME COURT LIMITS IEEPA AS A TARIFF AUTHORITY

A U.S. Supreme Court decision issued February 20, 2026 held that the International Emergency Economic Powers Act (IEEPA) does not authorize the President to impose tariffs.

In the same timeframe, the White House issued a set of tariff-related actions that (1) wind down IEEPA-based “additional ad valorem” duties and (2) establish a temporary import surcharge using a different statute: Section 122 of the Trade Act of 1974.

KEY SOURCES:

- Executive Order: Ending Certain Tariff Actions

- Proclamation: Imposing A Temporary Import Surcharge To Address Fundamental International Payments Problems

- Fact Sheet: President Donald J. Trump Imposes A Temporary Import Duty To Address Fundamental International Payment Problems

- Executive Order: Continuing The Suspension Of Duty-Free De Minimis Treatment For All Countries

ACTION 1: ENDING “ADDITIONAL AD VALOREM” DUTIES THAT RELIED ON IEEPA

A White House order states that the additional ad valorem duties imposed under IEEPA in a list of prior executive orders “shall no longer be in effect” and, “as soon as practicable, shall no longer be collected.”

What the order directs agencies to do:

- Begin immediate implementation steps and terminate collection of the specified IEEPA-based additional duties.

- Determine whether changes to the Harmonized Tariff Schedule of the United States (HTSUS) are needed and, if so, make updates via Federal Register notice.

What the order says it does not change:

- It applies only to the IEEPA-based “additional ad valorem” duties identified in the order.

- It does not affect duties imposed under other authorities, including Section 232 (Trade Expansion Act of 1962) and Section 301 (Trade Act of 1974).

- It also states that a separate executive order on continuing the suspension of duty-free de minimis treatment and the temporary import surcharge proclamation are unaffected.

ACTION 2: A NEW TEMPORARY 10% IMPORT SURCHARGE UNDER SECTION 122

A separate proclamation invokes Section 122 to impose a temporary import surcharge aimed at addressing “fundamental international payments problems,” including a cited balance-of-payments deficit rationale.

Core features (as described by the proclamation and fact sheet):

- Rate: A 10% ad valorem duty on imported articles, subject to stated exceptions.

- Duration cap: Section 122 is described as authorizing action for up to 150 days unless extended by an Act of Congress.

- Effective date/time: The fact sheet states the duty takes effect February 24 at 12:01 a.m. Eastern.

- End date referenced in the proclamation: The proclamation text references an expiration time on July 24, 2026 (Eastern Daylight Time) unless suspended, modified, terminated earlier, or extended by Congress.

HOW THE SURCHARGE INTERACTS WITH OTHER TARIFFS (SECTION 232 AND BEYOND)

The proclamation states the surcharge is generally in addition to other duties and charges—but not in addition to Section 232 tariffs. Where Section 232 applies to part of an import, the surcharge applies only to the portion not covered by Section 232.

It also states the surcharge:

- Is treated as a regular customs duty.

- Includes specific Foreign Trade Zone (FTZ) handling language (e.g., privileged foreign status requirements for most covered articles admitted to FTZs on/after the effective date).

EXCLUSIONS AND CARVE-OUTS HIGHLIGHTED BY THE WHITE HOUSE

The fact sheet lists categories of goods that “will not be subject” to the temporary import duty, citing economic needs and targeted design considerations.

Examples include:

- Certain critical minerals, energy and energy products, and certain metals used in currency and bullion

- Certain natural resources and fertilizers not produced (or not produced sufficiently) domestically

- Certain agricultural products (examples listed include beef, tomatoes, and oranges)

- Pharmaceuticals and pharmaceutical ingredients

- Certain electronics

- Certain vehicles and related parts (multiple vehicle classes referenced)

- Certain aerospace products

- Informational materials (e.g., books), donations, and accompanied baggage

Additional exclusions in the fact sheet include:

- Articles currently (or later) subject to Section 232 actions

- USMCA-compliant goods of Canada and Mexico

- Certain textiles/apparel entering duty-free under CAFTA-DR country rules cited in the fact sheet

De minimis: low-value shipments are referenced as part of the implementation picture

The fact sheet states that the White House also continued the suspension of duty-free de minimis treatment for low-value shipments (including goods shipped through the international postal system) and notes those shipments “will also be subject” to the temporary import duty imposed under Section 122.

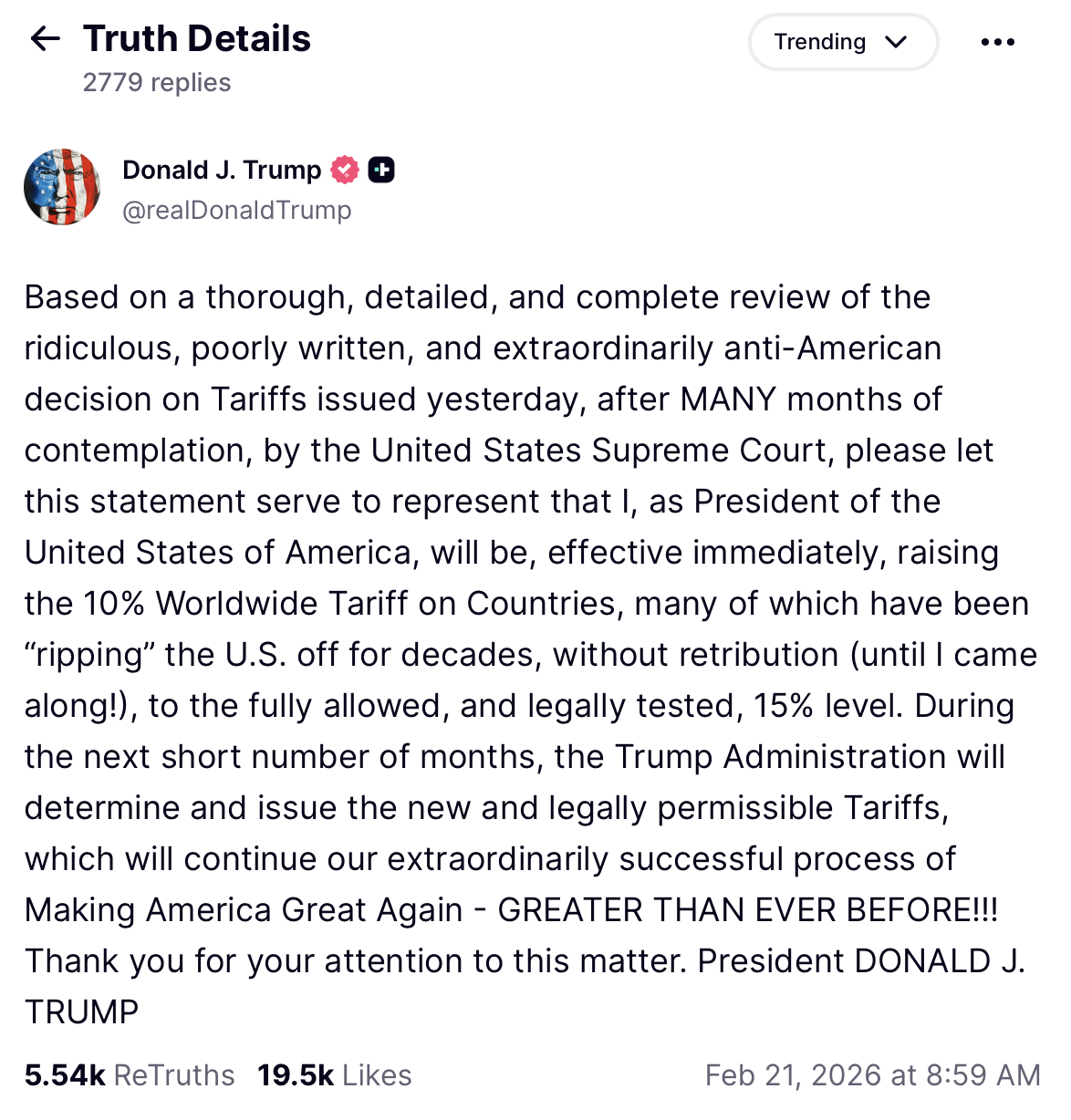

SURCHARGE INCREASE FROM 10% TO 15% ALREADY?

A February 21, 2026 social media post from the President states an intent to raise the temporary 10% worldwide import duty to 15% “effective immediately,” and indicates additional tariff steps may follow in the coming months; however, as of this writing, that statement has not been substantiated by a corresponding White House executive action or an official update to the proclamation establishing the temporary import surcharge.

Stay up-to-date on freight news with Green’s Weekly Freight Market Update by following us on LinkedIn. For continuous updates, make sure to check out our website at greenworldwide.com.